All the things that changed on 1 July (and what it means for you)

And, in the Nine Newspapers this weekend "Our super system has a new blind spot, and it could cost you thousands"

In this edition: It’s a juicy one

Feature: All the things that changed on 1 July (and what it means for you)

From Bec’s Desk: A long list of cool stuff going on

The Age and Sydney Morning Herald: Our super system has a new blind spot, and it could cost you thousands

Prime Time: Protecting your retirement savings: an important warning

Ad - Right on time - our next Epic Retirement flagship course has gone on sale

Retirement doesn’t come with a manual.

But it does come with an 8.5-hour course, with 15 modules, 6 live Q&As with some of Australia’s sharpest retirement minds, a 150-page workbook mailed to your door, and a cohort of people doing it exactly alongside you.

The Spring edition of the How to Have an Epic Retirement Flagship Course kicks off 13 August and the 25% earlybird deal is on now, for the first 200 people.

It sells out. It gets rave reviews. And it’s just been fully updated with every change that landed on July 1.

If you’ve been thinking you might - nows the day to book.

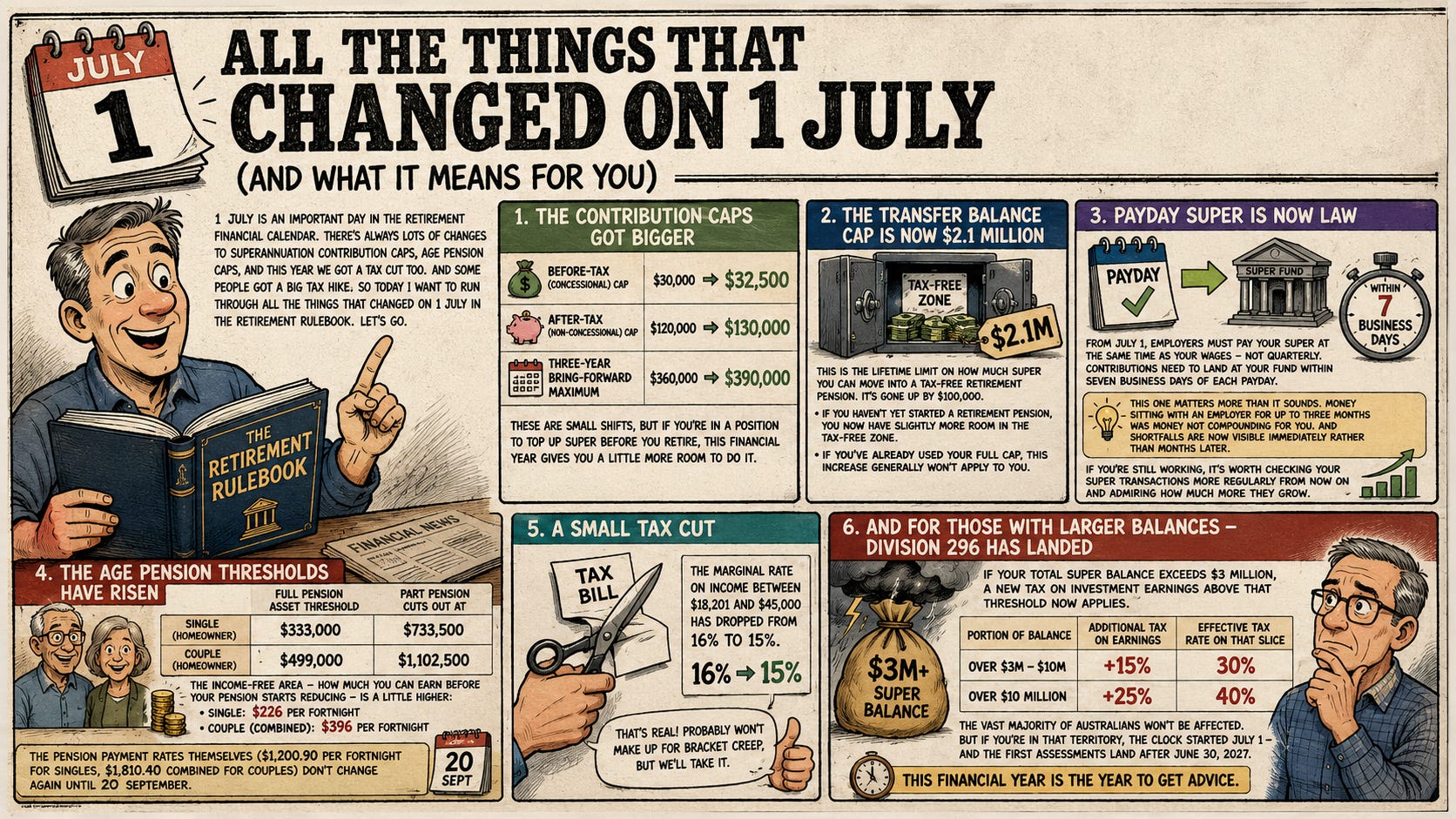

All the things that changed on 1 July (and what it means for you)

1 July is an important day in the retirement financial calendar. There’s always lots of changes to superannuation contribution caps, age pension caps, and this year we got a tax cut too. And some people got a big tax hike. So today I want to run through all the things that changed on 1 July in the retirement rulebook. Let’s go.

The contribution caps got bigger

The before-tax (concessional) cap has moved from $30,000 to $32,500. The after-tax (non-concessional) cap goes from $120,000 to $130,000. And the three-year bring-forward maximum is now $390,000, up from $360,000.

These are small shifts, but if you’re in a position to top up super before you retire, this financial year gives you a little more room to do it.

The transfer balance cap is now $2.1 million

This is the lifetime limit on how much super you can move into a tax-free retirement pension. It’s gone up by $100,000. If you haven’t yet started a retirement pension, you now have slightly more room in the tax-free zone. If you’ve already used your full cap, this increase generally won’t apply to you.

Payday super is now law

From July 1, employers must pay your super at the same time as your wages - not quarterly. Contributions need to land at your fund within seven business days of each payday.

This one matters more than it sounds. Money sitting with an employer for up to three months was money not compounding for you. And shortfalls are now visible immediately rather than months later. If you’re still working, it’s worth checking your super transactions more regularly from now on and admiring how much more they grow.

The age pension thresholds have risen

The full pension asset threshold for a homeowner single is now $333,000, with the part pension cutting out at $733,500. For homeowner couples, those figures are $499,000 and $1,102,500.

The income-free area - how much you can earn before your pension starts reducing - is a little higher at $226 per fortnight for singles and $396 combined for couples.

The pension payment rates themselves ($1,200.90 per fortnight for singles, $1,810.40 combined for couples) don’t change again until 20 September.

A small tax cut

The marginal rate on income between $18,201 and $45,000 has dropped from 16% to 15%. That’s real! Probably won’t make up for bracket creep, but we’ll take it.

And for those with larger balances - Division 296 has landed

If your total super balance exceeds $3 million, a new tax on investment earnings above that threshold now applies. Earnings between $3 million and $10 million attract an additional 15%, making the effective rate 30% on that slice. Above $10 million, the additional rate is 25%, making it 40%.

The vast majority of Australians won’t be affected. But if you’re in that territory, the clock started July 1 - and the first assessments land after June 30, 2027. This financial year is the year to get advice.

Want to read more, I have two books - How to Have an Epic Retirement and if you’re not ready for retirement, Prime Time: 27 Lessons for the New Midlife.

Hey there! So many little titbits this week I’m going to break things up with a few headings to make sure I share all the good bits. And make sure you read my Sydney Morning Herald article and listen to the podcast - I had the ASIC Commissioner Simone Constant on to talk about platforms, and the holes that need plugging in their oversight of advisers. This stuff is important. I’ve tried to make it easy to grasp.

Now - onto the action-face.

The Spring Program has launched

It’s here! Our new Spring edition of the How to Have an Epic Retirement Flagship Course has officially gone on sale at the 25% off earlybird price.

It’s a six week program, designed to help you step through 8.5 hours of retirement lessons, about everything you need to understand to navigate retirement with confidence.

It’s a course that gets rave reviews. And we only run it four times a year. And last time we completely sold out (of books and workbooks) so we had to shut the doors early!

The new program has been fully updated with all the new changes that arrived this week. We’ve also launched a new website, so you can pop on over and read all about it, and book your place.

There’s a 25% off Earlybird Deal on now, for the first 200 people who book. So get in there, check out all the inclusions (it’s a huge list) and lock down your place as they sold out well and truly last time. There’s also a detailed brochure you can download.

HESTA Epic Retirement Program

We’re launching a new Epic Retirement program for HESTA members in the next week or so. So if you’re a HESTA member - keep your eyes peeled on their member emails to you. It’s a great course. You need to be a member of HESTA to access it. And there’s limited places - so don’t dilly dally!

Melbourne rightsizing event

I’ll be heading to Melbourne next week for a really interesting event on downsizing into luxury apartments. I’m excited. The event is being held by Lowe Living. If it interests you - click here to learn more and register your place. I’m speaking with the property economics gurus from Urbis.

Aware Super couples event

I’ve got a fun event coming up in three weeks time - all about planning for retirement as a couple. If you’re an Aware Super member - make sure you keep an eye out for it and register your place.

An Epic Start

Many of you will have seen that my daughter Paris and I have started something new together.

It’s called An Epic Start, and it’s a social media channel where we talk through the financial basics that young adults actually need to know. Banking. Super. The First Home Super Saver Scheme. Home deposits. How to think about buying a home. Basic investing. The rules of money that nobody teaches you at school - and that most parents aren’t sure how to explain.

Paris is 22. She lives in the real world, works three part time jobs while studying at uni, and has real questions. She’s been backpacking - and she’s home, ready to start her life, maximising her opportunities. And the content space aimed at people her age is - to put it plainly - a mess. Finfluencers flogging ETF platforms. Mortgage brokers collecting referral fees. People making money look easy in ways that aren’t always honest.

That’s not what we’re doing.

An Epic Start is facts. How things actually work. What you need to know. No products to sell, no affiliate links, no agenda beyond giving young people a genuinely epic start.

If you have adult kids or grandkids navigating this stuff, send them our way. We’re on Instagram at instagram.com/an.epic.start and TikTok at tiktok.com/@an.epic.start. (We’re on Facebook too here).

Paris and I are having the best time building this together. Some things are worth doing just because they matter.

—

And the Epic Bucket List Holidays (see that - I renamed them)

Last week I shared a long dream about taking commmunity trips to bucket list destinations, and I invited you to express your interest. Well hundreds of you did! And now, we’re working on the potential destinations for year 1. Fiona Dalton, the Epic travel guru is leading the way on this, picking the best adventures.

I mean real handpicked bucket list stuff. Active and experience-first. And never the same destination twice. If you’re on the EOI list, we’ll be emailing you a wish list to explore what you’d want to do out of our ideas, in the week ahead. And if you haven’t put your name on the list yet - Express your interest here - no obligation.

Now I’m taking a few days off. Shhh - hope you don’t notice. Until next week - make it epic! Cheers Bec xx

Author, podcast host, columnist, retirement educator, and guest speaker

Our super system has a new blind spot, and it could cost you thousands

If you have a financial adviser and your superannuation investments are being managed on something called a platform, there are some important things to look at this week.

Australia’s financial regulator, ASIC has just released a report that found some serious gaps in the way our major platforms are safeguarding members’ money. The findings are concerning enough that ASIC brought them to me to explain to you simply, so you’re more aware of them.

Basically, investment platforms are meant to have processes, monitoring and caps in place to stop shonky advisers or dodgy investment businesses from taking advantage of unknowing consumers. ASIC has repeatedly asked the platforms to take their responsibilities as trustees seriously, driving for three big obligations.

Firstly, to keep Australian superannuation money invested in their platform safe, especially from bad conduct. This means platforms need to carefully vet the investments they offer and ensure no bad actors can use them as a vehicle to take advantage of members.

Secondly, to make sure that Australians are getting genuine value for money for the services being paid for out of their super and that members actually understand what those services are. And finally, to deliver investment, member and retirement services that sit at the heart of what a superannuation trustee is to provide.

Those three obligations sound pretty reasonable when you say them out loud. They’re not complicated or tricky. But when ASIC reviewed six of Australia’s largest platform trustees recently, organisations that are responsible for safeguarding $400 billion of retirement savings, across all three of those expectations there were serious and persistent failings.

This article continues… It is published in The Age and Sydney Morning Herald on Saturday 4th July 2026. Read the whole article here, without a paywall.

This week, I sit down with ASIC Commissioner Simone Constant to unpack a deeply concerning new report exposing major flaws in the safety nets legally required to protect Australians’ retirement savings.

ASIC reviewed six platform trustees responsible for more than $300 billion in retirement savings and found persistent failures in areas such as monitoring advice fees, unusual investment patterns, and high-risk super switching. The regulator has made it clear: trustees need to do better, and quickly.

If you have your super managed by a financial adviser through a platform product, this is an important conversation. We discuss what the report found, why it matters, the responsibilities trustees have to protect your money, and the exact questions you should be asking your adviser today.

Your super is likely to be one of the biggest assets you’ll ever own. Understanding where it is, why it’s there and how it’s being protected has never been more important.

You can find the report from ASIC here and I’ll be doing a deep dive in this weekend’s newspapers.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Loved the comical caption you have delivered it with!