The retirement date you pick vs the one life picks for you

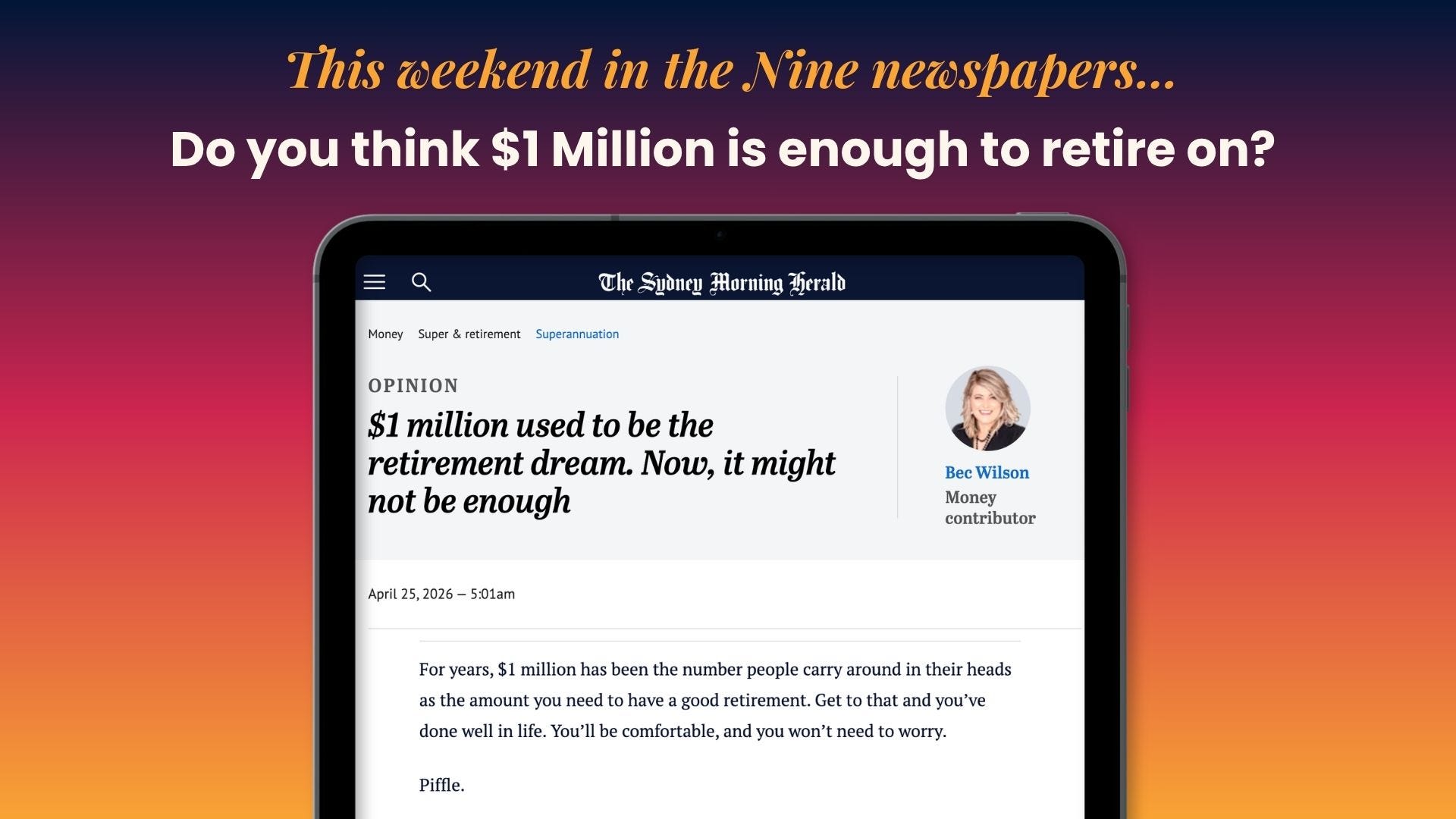

And in the weekend newspapers: '$1 million used to be the retirement dream. Now, it might not be enough'

In this edition

Feature: The retirement date you pick vs the one life picks for you

From Bec’s Desk: On the road again!

The Age and Sydney Morning Herald: $1 million used to be the retirement dream. Now, it might not be enough

Prime Time: Could you stop working tomorrow… and still get paid?

But first, an ad for our upcoming course…

Last chance to secure an Earlybird ticket!

Our next program kicks off on 14 May, and our Earlybird deal (25% off) is now open—but places are limited. Hundreds of people have already booked and this is on track to be the biggest Epic Retirement Course yet!

This is a six-week retirement education program designed to build your confidence and help you make sense of the many decisions ahead.

Learn more about the course here ➡️

The retirement date you pick vs the one life picks for you

Most people have a number in their head. Maybe it’s 62. Maybe 65. Maybe “when the mortgage is paid off” or “when the kids are sorted.” It’s the date you’ve been quietly working toward – the finish line you’ve drawn in pencil on the wall of your mind.

But here’s a stat that tends to stop people in their tracks: only 31% of Australians retire by choice. The rest are pushed, by redundancy, by health, by a partner’s illness, or by a workplace that quietly makes it clear their time is up.

That means roughly two in three people don’t get to retire on their own terms. Life picks the date for them. This isn’t meant to be alarming information. It’s meant to be useful.

The gap between planned and actual

There’s often a significant gap between when people expect to retire and when they actually do. And that gap almost always runs in one direction – earlier than planned. An unexpected redundancy at 58. A health scare at 61. A parent who needs care, a partner who can’t wait, a job that disappears in a restructure.

When retirement arrives ahead of schedule, people who have a plan adapt. People who were counting on “a few more years” to get ready can find themselves scrambling.

What you can control

You can’t always control when you leave work. But you can control how prepared you are when it happens. A few things worth thinking about now:

Know your numbers today, not later. What would your retirement actually look like if it started next year? Run that scenario: super balance, likely pension eligibility, expenses. Even a rough picture is better than none.

Don’t put all your preparation into the final years. It’s tempting to think “I’ll sort the finances when I’m closer.” But if those final years get cut short, you want the groundwork already done.

Think about your non-financial readiness too. Identity, purpose, routine, social connection – these things really do take time to figure out. People who’ve thought about what they’re retiring to, not just from, tend to land better when the transition comes unexpectedly.

Consider a gradual exit. Moving to part-time or consulting before you fully retire gives you a trial run and keeps income flowing longer, which buys flexibility.

The silver lining

Here’s what I’ve seen again and again: people who are nudged into retirement earlier than planned often adjust faster than they expected. The fear of it is usually worse than the reality. Especially when the basics are in place.

The goal isn’t to panic about what you can’t control. It’s to make sure that whenever that date arrives – whether chosen or not —–you’re not starting from scratch.

Plan like it could happen sooner than you think. Hope it doesn’t. Either way, you’ll be ready.

The Epic Retirement course and/or book walks you through exactly this process building your own retirement picture step by step, so you can move from worry to excitement about your retirement.

Get your copy of my books here: How to Have an Epic Retirement and if you’re not ready for retirement, Prime Time: 27 Lessons for the New Midlife.

Or explore the course here: Epicretirement.net/upcoming-courses

I’ve been on the road all week keynoting the AMP North Adviser Roadshow through its biggest cities in Sydney and Melbourne. It’s so much fun! The adrenaline is addictive. The energy is fabulous. I love it when people queue up to get a copy of the book after too. I’m talking to Advisers about how important it is help people have not just an Epic Retirement, but a Prime time too, and how that Prime Time can be structured, into a setup phase, a lifestyling phase, and a part-timing phase. Lots of nodding heads and agreement from them! Which is terrific. Next week I’m off to do it all again in Adelaide and Perth.

In other things, this week our podcast was awesome - I hope you’ve had a listen. It was two people - Xavier O’Halloran from Super Consumers Australia and Kate Rolfe from Aware Super - talking about layering your super and the age pension.

And we’ve seen the How to Have an Epic Retirement Course hit awesome new heights. This is going to be the biggest course ever. I’m holding Earlybird 25% off open for a couple more days. Don’t delay though - I have to close it very soon to place the final book orders and get them in the mail.

On the side of all my Epic Retirement work, I’ve been loving every minute of working with my daughter, Paris, on An Epic Start - helping her learn how to budget, save, and invest. We’ve each been making little videos for Instagram and Tiktok to help adult kids and their parents learn the ‘new stuff’ we all need to know (us and them) so our kids can have an epic start. So much of investing, home buying and starting out has changed since we did it. Come and follow the channel (I’m super impressed at the videos Paris is making - making it real for all the younger gen).

More here:

And if you have adult kids starting out - tell them about it please. We want to help!

Now, on with the Sunday - make it Epic!

Cheers Bec

Author, podcast host, columnist, retirement educator, and guest speaker

$1 million used to be the retirement dream. Now, it might not be enough

For years, $1 million has been the number people carry around in their heads as the amount you need to have a good retirement. Get to that and you’ve done well in life. You’ll be comfortable, and you won’t need to worry.

Piffle.

What I’m seeing now is that more people are getting close to that figure, or even reaching it, and instead of feeling secure, they feel uncertain. They’re not stressed, and they’re not struggling, but they’re certainly not as confident as they expected to be that they have enough.

And the reason is pretty simple. The number hasn’t kept up with how retirement actually works any more.

A million dollars in super still puts you in a strong position. But when you translate it into income, it starts to look very different from the old idea of being “set for life”.

This article was published in The Age and The Sydney Morning Herald on Saturday 25th April 2026. Read the whole article here. Note - it has a sign-up gate but no paywall.

We spend our working lives earning an income. But at some point, the game changes completely.

The paycheck stops. And suddenly we’re not earning an income from full time work anymore, instead, we need to learn how to manage a more passive set of income streams. Super, the Age Pension, maybe a bit of work, some investments on the side. And for each layer, there’s different sources, different rules, and different timing. All of it needs to work together to replace the one simple income most people had before.

And that’s where most people get caught out. It’s not because they haven’t saved enough. It’s simply because nobody ever taught them how to actually run this thing called retirement.

This week on Prime Time, I sit down with Xavier O’Halloran from Super Consumers Australia and Kate Rolfe, Head of Retirement Strategy at Aware Super. We get into the real mechanics of layering a retirement income; what the sources are, how they shift across different phases of retirement, and how to build a picture that actually works for your life.

In this episode we also discussed the Super Consumers Australia’s Retirement Savings Targets. You can find them here.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

In Canada, the major banks are using $1.4 million dollars as the amount needed for retirement. But how many retirees do you know who have that amount of money? Financial advisors often latch onto the $1.4 million figure, then of course most advisors don't want clients with less than $500,000 in liquid assets.

The average Canadian's retirement savings is around $272,000 in cash or about $517,000 in total retirement assets :(including pensions/RRSPs)

So, how much is enough? I've advocated for pre-retirees not to concentrate on amassing an abnormal amount of wealth, but to determine how much money will make them feel secure. In others words, how much money do you need to enable you to live and fulfill your visualized retirement lifestyle?

In a practical sense, how you spend your retirement time determines how much money you will need. If you plan to travel the world or indulge in expensive hobbies such as luxury sailing, then your financial needs will be much greater than someone with more modest plans. What you don't want is to envision a retirement you realistically cannot afford. Financially estimating your retirement plans is the key to determining the amount of money required.

For more information and insights, visit my website: whencaniretire.ca

Here's the fact: I'm a bit of an expert on retirement, not because I've been retired for eight years already, but because I have a wonderful lifestyle. I live life on my terms, and a long time ago I decided I didn't want to spend my retirement in the dull UK, huddled by the radiator all winter.

All of my family have always enjoyed the sun. If we had a spirit animal guide, I'm sure it would be a lizard, because when the sun comes out, we run out and warm up and enjoy it. For that reason, I decided I wanted to spend my winters in a warm place and enjoy perpetual summer. That, plus I married a Philippine lady. I decided to spend from mid-September till mid-May living in the Philippines, and that's what I do. After that, I return to the UK.

2025 was a beautiful summer. Not sure what this one's going to be, but anyone can have a wonderful retirement. Here's the big thing you're probably thinking: I have loads of cash. Not as much as you might think.

Living here in the Philippines is not expensive, and if you follow a few simple rules, you can live abroad quite cheaply for the whole of the winter period. After all, unless you like the fog, the rain, and the cold, what's the point of staying in the UK in the winter? Christmas, that lost its appeal a long time ago.