How a low super balance can still mean a happy, fulfilling retirement

And in my feature: Four smart steps to take with your super this weekend. Plus we're having fun demystifying retirement jargon for you

In this edition

Feature: Four smart steps to take with your super

From Bec’s Desk: Back on home soil

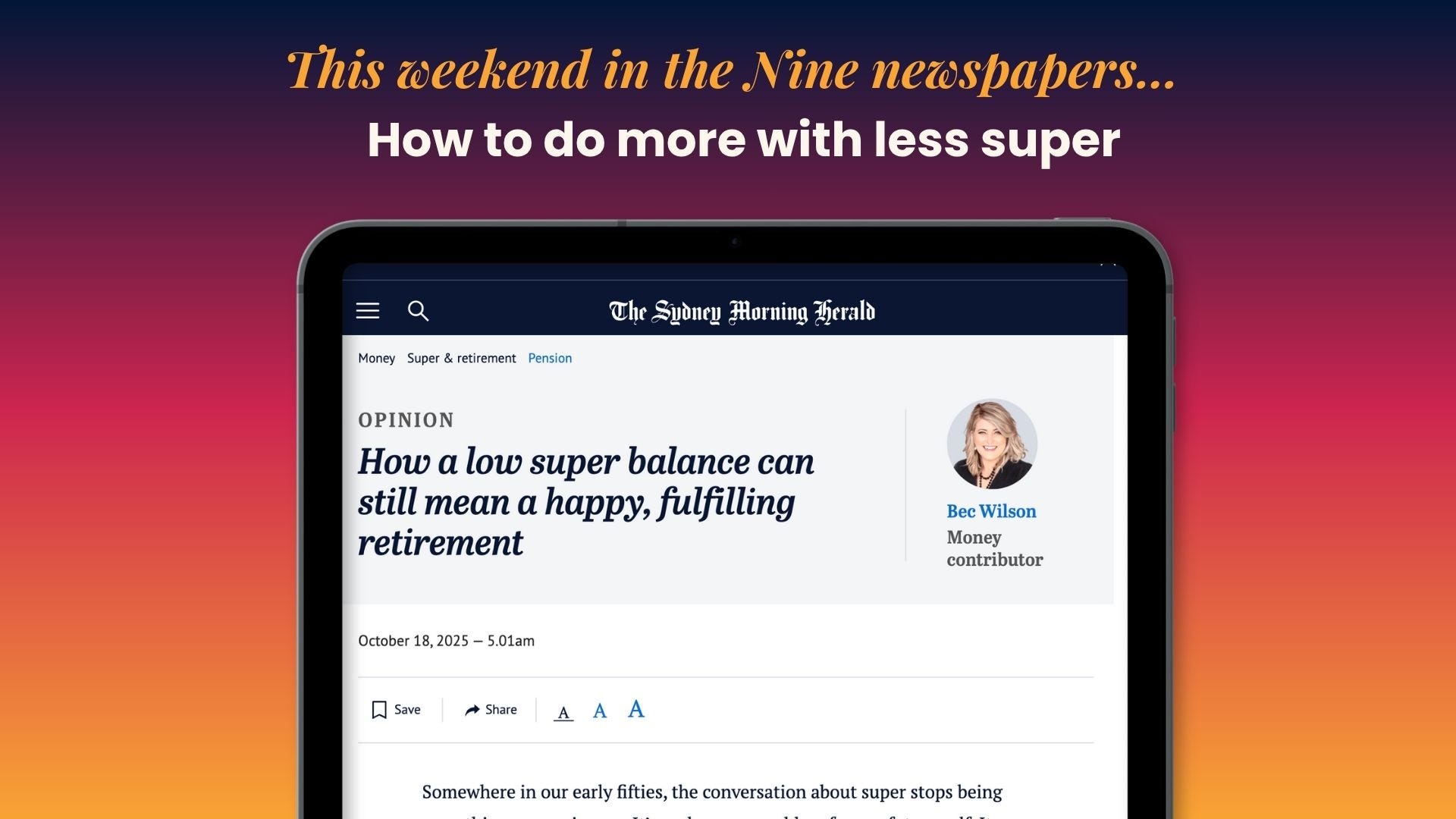

SMH/TheAge: How a low super balance can still mean a happy, fulfilling retirement

Prime Time: Retirement jargon demystified: All the terms you NEED to know

Ad - Before we start — a big thanks to our newsletter sponsor this week, Viking

Join Viking’s Free Online River Voyage Information Session: Grand European Tour

On Thursday 23 October at 11:00am, Viking is hosting a live virtual event where experts will guide you step by step through their popular Grand European Tour river voyage. You’ll discover port highlights, learn about popular excursions and life onboard, and get a taste of this unforgettable journey. Think medieval castles, Gothic cathedrals, vineyard-covered hillsides, lively market squares and more.

We’ll also share practical tips, personal anecdotes, and recommendations to inspire your travel planning. If you are thinking of taking a river cruise along the Rhine or Danube, this is an event you shouldn’t miss.

Four smart steps to take with your super

I’ve just come back from the UK, where the pensions industry is in full-blown worry mode. Everyone – from policymakers to fund managers – is anxious about whether ordinary people will be able to retire with enough to live in comfort. The problem? Most people are only obligated to contribute 8% in the UK and that’s leading to pots that are too small to help people retire well.

In contrast, Australia’s super system is world-class and we’ve worked our way up to 12% contributions this year, but we need more people to learn how to use their funds as they head for retirement - an important step to take. Too many people are drifting toward retirement without understanding how their super’s performing, what they’re paying in fees, or how to turn a balance into an income stream that will last for the rest of their life.

And when you ignore it, or stick your head in the sand your overall retirement confidence drops – not because the system’s broken, but because people stop trusting what they can’t see.

We should all be aware that retirement is a self-help stage of life. No one’s coming to fix it for you – not your fund, not your employer, not the government. If you want a good retirement, you have to get curious, start asking questions, and work out whether your fund is setup to help you.

Here’s how to start taking a closer look.

1. Know what you’ve actually got

Don’t just look at the number – take the time and make the effort to understand it.

Log in to your super fund and check: what’s your balance invested in? What returns has it earned in the last five or ten years? What are the fees? How much insurance are you paying for, and do you still need it? You can’t control markets, but you can control what you’re invested in and whether it suits your stage of life.

2. Make your money work smarter, not harder

If your fund’s underperforming, high-fee, or just not transparent – move it. Rolling over to a better-performing fund with solid services for pre-retirement and retirement can make a massive difference over a decade. Even small improvements in fees over the long term or more stable long term returns can add tens of thousands of dollars to your retirement income simply through compounding.

3. Turn your balance into an income plan and projection

You don’t retire on a lump sum – you retire on what that lump sum pays you.

So take some time to learn how your super turns into income. Use your fund’s calculators or online tools to see what your current balance might provide each month. If it’s not enough, work out what small changes – like salary sacrificing, or catching up with extra contributions in your 50s, could get you closer to the life you want.

4. And check if your fund has the Epic Retirement tick

We’ve created 18 criteria, and assessed Australia’s superfunds against them to determine whether they are doing enough for their members as they approach retirement. It’s called The Epic Retirement Tick powered by Chant West - and you can download the report and see if your fund is retirement ready here.

Next time you glance at your super, don’t just look at the number — look deeper. Ask yourself: is my fund really good enough to earn the Tick?

Hey everyone. A short one today. I’m back on Aussie soil after two weeks in the UK. A little tired, but after a good sleep I’ll be ready for the next burst of excitement. We’ve just kicked off the Hesta Exclusive Edition of the Epic Retirement Course for almost 1000 HESTA members - a completely full course to pilot their special program. It’s hopping with action too. So nice to see.

And our next How to Have an Epic Retirement Flagship Course is just three weeks from kickoff - not long now! Book your place if you’re keen for a 25% earlybird spot as they are almost gone. And know this - it’s a revised program, and we’re getting an advance shipment of my new ‘updated and improved’ edition of How to Have an Epic Retirement the book to ship to you earlier than they’re available in stores. So if you’ve registered, know the books will come in the very last days - as we’re waiting on the print run for the welcome packs. Find out more here.

I head to Melbourne this week for a series of different corporate events and if you’re keen to come to an event I’ll be heading to Clyde in Victoria for a speech about the ‘6 pillars of an Epic Retirement’ for Lifestyle Communities.

Date: 22nd October 2025 10am-12pm;

Location: Lifestyle Communities Riverfield; 25 Concerto Street, Clyde

Learn more here and book your spot.

And finally - be sure to listen to this week’s Prime Time podcast with David Bell. He’s a good sport! We talk all about the fun jargon you get from funds and how to navigate it.

The new UK and Australia/New Zealand editions of Epic Retirement are coming - November and December are set to be big Epic Retirement months. And, in the meantime, Prime Time: 27 Lessons for the New Midlife is still going super-strong I’m pleased to say, helping those who aren’t yet ready to retire to dive into a better midlife (and still set themselves up for an epic retirement later)!

And that’s it - enough for a Sunday. Now get on in and have a look at your super this weekend - it’s worth doing, then making it a semi-regular check.

Until next week, make it epic!

Author, podcast host, columnist, retirement educator, and guest speaker

Extract of of my weekly column in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 19th October 2025.

How a low super balance can still mean a happy fulfilling retirement

Somewhere in our early fifties, the conversation about super stops being something we can ignore. It’s no longer a problem for our future self. It starts to feel close, real, and awfully personal. Many of us begin doing quiet maths in our heads:

“Have I saved enough? Am I where I should be?” Then we see headlines saying Australians need half a million in super to retire comfortably, and we feel a pang of doubt.

The reality is that most people in their fifties or early sixties have far less than that, and it doesn’t make them unable to retire. It makes them typical Australians approaching retirement.

The latest ATO data shows the median super balance for Australians aged 60-64 is $219,773 for men and $163,218 for women. For people aged 50-54, the figures fall to $177,194 for men and $122,150 for women.

These figures from the 2022-23 financial year represent the real middle ground of Australian retirement. Half of people have less, and half have more. If you’ve been comparing yourself with the glossy headline numbers, it’s easy to feel like you’ve fallen short. But in reality, these balances can still be a solid foundation, especially if you start acting early and build a plan around what you have.

Read on — this article continues in The Age, The Sydney Morning Herald,Brisbane Times and WA Today. It is free to read - you may have to sign up, but there’s no paywall on my articles.

Retirement jargon demystified: All the terms you NEED to know

Have you ever read something from your super fund… and thought, I have no idea what that means?

You’re not alone.

In this week’s episode of Prime Time, I’m joined by David Bell, Executive Director at The Conexus Institute and co-author of a recent paper that analysed retirement income forms from 20 of Australia’s biggest super funds. The results? Let’s just say… not exactly straightforward.

Together, we explore why there are so many confusing names for what’s essentially the same thing (flexi pension, choice income, pension account — take your pick), why the language doesn’t line up across tools and forms, and how it all impacts your ability to make good decisions about your retirement income.

Until the industry agrees on a clear dictionary, my advice is this: don’t be afraid to ask your fund to explain things in plain English. It’s your money, after all — and you deserve to understand how it works.