The retirement tool the industry doesn’t want you using (but you already are)

And in this weekend's newspapers: 'Not ready to stop work or retire? You’re not alone'

In this edition

Feature: The retirement tool the industry doesn’t want you using (but you already are)

From Bec’s Desk: A new project I am curious about your interest in

The Age and Sydney Morning Herald: Not ready to stop work or retire? You’re not alone

Prime Time: Finding meaning outside of work

The retirement tool the industry doesn’t want you using (but you already are)

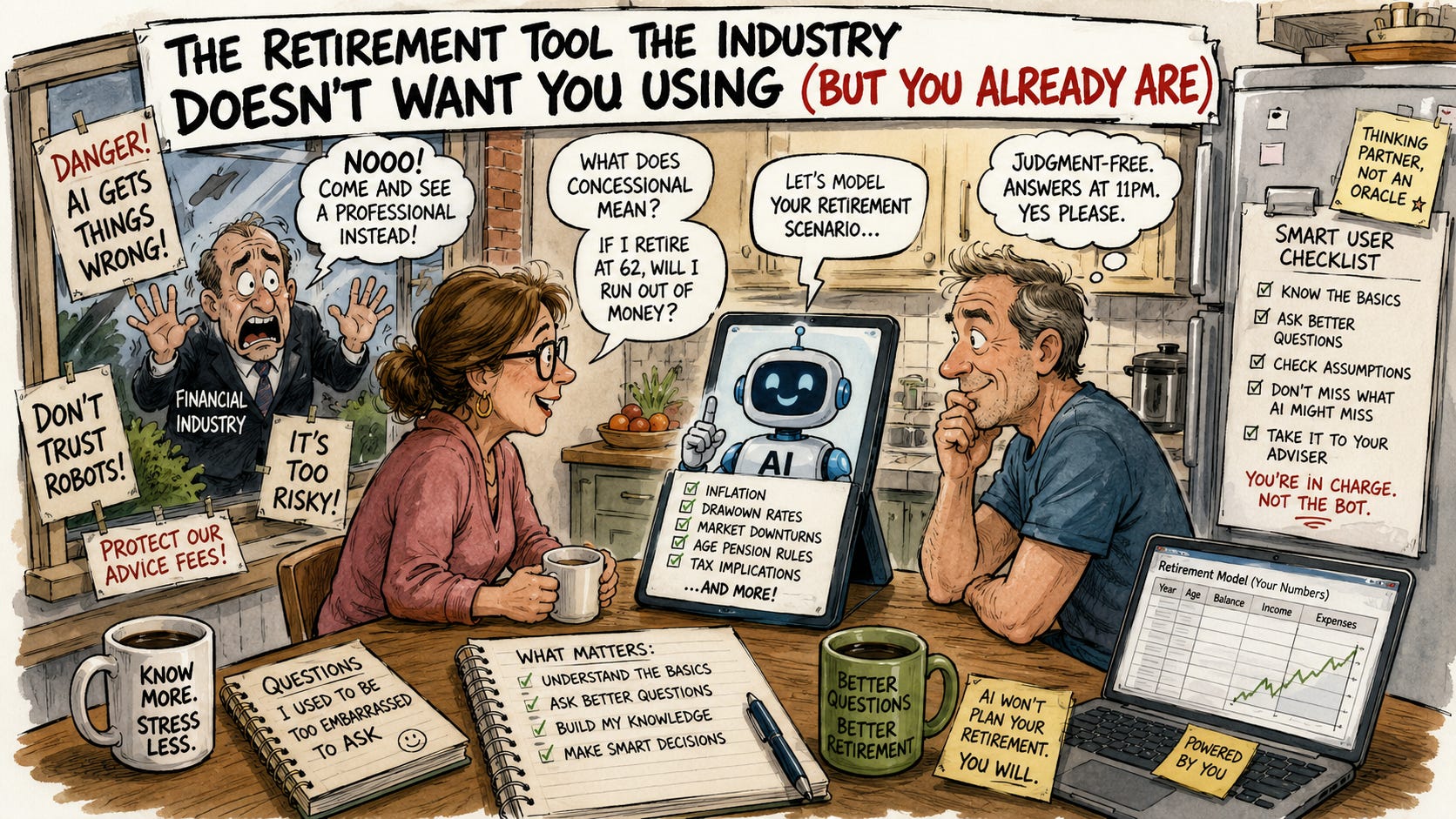

Something is happening at kitchen tables across Australia, and the financial advice industry is losing its mind, loudly, about it.

People are asking AI about their retirement. How much money they need, and how to invest, and how to plan for it. They’re even asking Claude to build Excel-style financial models, and it can do that straight from the ordinary chat window, no special setup needed.

They’re not asking their adviser first, or their superfund hotline, or even their brother-in-law who works in finance and holds court at Christmas. They’re opening up ChatGPT or Claude on their phone and typing the questions they’ve been too embarrassed to ask anyone: What does concessional mean? Is my super actually being invested well? If I retire at 62, will I run out of money?

Let’s face it - that last question matters and there’s a particular kind of shame that comes with not understanding your own financial situation in your 50s, when you feel like you should have it sorted by now. AI gives people a judgment-free place to start asking questions and building understanding.

And here’s where I part ways with most of the financial industry on this. I love it. The agency it gives you to be curious and consider things from different perspectives is powerful. The fact it can build you a genuinely useful spreadsheet, one you can fill in with your own numbers and take straight to your adviser, is nothing short of fabulous.

The standard adviser response to AI is some version of “be careful, it gets things wrong, come and see a professional instead.” And yes - AI does get things wrong. I catch it out all the time. It uses old data, leaves a critical number like inflation out of a calculation or a spreadsheet, or simply doesn’t grasp the interplay between the age pension and super - unless you prompt it to. I push back, ask it to check things, or feed it the correct facts straight from Centrelink, and you need to be aware of those limitations if you use it.

There’s lots of studies being done on this. In one study, it gave incorrect or incomplete answers to about a third of the financial questions it was asked. Worth knowing as you go in.

So let me be clear. It probably doesn’t know your full picture. And without it, it can’t model your real tax situation, and even with it - I’d be worried you left something out. It has blind spots around things like sequencing risk and aged care costs that could actually hurt you if you act on its answers without understanding what’s missing.

But the solution to that isn’t to avoid AI. It’s to know enough that you’re not dangerous when you use it.

Here’s what I mean by that. If you ask AI “will I have enough to retire?” and you don’t know what questions to follow up with - about drawdown rates, about inflation, about what happens if markets fall in your first few years of retirement - you’ll get a confident-sounding answer that might be wrong in ways you won’t spot. AI doesn’t volunteer what it left out. It answers what you asked. If it was a simple question you might get an overly simplified answer.

But if you understand the basics? Suddenly you’re having a completely different conversation. You’re the one steering. You’re asking better questions, pushing back when something doesn’t add up, and using AI the way it’s actually meant to be used - as a thinking partner, not an oracle.

That’s always been the whole point of what we do here with education. Not to replace professional advice, but to give you enough understanding to be a smart consumer of every resource available to you. So that when you talk to your super fund, you know what to ask. When you see a financial adviser, you understand what they’re telling you. And yes - when you open up Claude at 11pm with a question you’ve been sitting on for months, you know how to make that conversation count.

So use the tools and ask the questions you’ve been too embarrassed to ask. Just make sure you’re building the knowledge alongside it, so you’re the one in charge of your retirement decisions, not the AI bot. Because that could get messy.

I’m smiling ear to ear this week because the mid-course feedback rolling in on our Australian and UK Epic Retirement courses, both running right now, is just so good. I feel incredibly proud of our six-week retirement education program which just keeps getting better.

It’s the main part of what we do here at the Epic Retirement Institute: helping people understand how retirement actually works so they can make better decisions and feel more confident about the future with a 6-week course.

Humour me while I share some of the shorter comments:

“The course is fantastic: so clearly and well structured. Thank you”

“We love this course content and the structure of it - will be recommending it to others!”

“I’m really enjoying the course, I think it should be government funded for all people in Australia age 50 plus.”

“This course has changed my life!!”

“I have been enjoying this course immensely. I feel much more confident in my understanding of how this thing called retirement works!”

That's the kind of confidence I want people to have. It's the same reason we built the Epic Retirement Tick, so you can work out whether the service you're getting from your super fund is genuinely delivering on performance, fees and service, or whether it's time to start asking some tougher questions as you head for retirement, and you can download the report here: www.epicretirement.net/epictick

I’m extremely tempted to put together some kind of assessment similar to the Epic Retirement Tick to help people consider their options for and evaluate financial advice and the investment management process as they head for retirement advice - what do you think? Would that be useful?

We’re not government-funded consumer advocates or anything, just aware that there’s really no one else in the retirement space who doesn’t make money from selling you a financial product or service, and who can have your education about all the choices available to you as the priority. But we don’t want to waste time on projects you won’t use. So help us filter the ideas - please!

Now, back to your Sunday programming! Our next epic retirement course is kicking off in August - so plenty of time to talk about it next week! You can register your interest for the Earlybird 25% off deal here.

Make it epic!

Cheers - Bec Xx

Author, podcast host, columnist, retirement educator, and guest speaker

Not ready to stop work or retire? You’re not alone

We have all inherited a traditional idea of retirement and frankly I think we need to push on its boundaries because it really was designed for a different era.

Retirement was created in the early 1900s to get old people out of the workforce where they were slowing down the factory lines. Most people who made it to retirement arrived in poor health and didn’t survive long enough to enjoy it.

Then, over the next hundred years, it morphed to become a period of life: one where we largely expected to live a more quiet existence in old age, on a pension. But even that idea has been thwarted.

Thanks to longer lives and superannuation, retirement today is a multi-stage period of life that could last 30 to 40 years. On average, just a quarter of that time will be spent in poorer health.

A 65-year-old woman today is expected to live to 90 at the median and she has a one in four chance of living to 95. A 50-year-old should expect an even bigger bounty: a median life expectancy of 91, and a one in four chance of getting to 97, which will surely expand in their lifetime. That’s not a wind-down at the end, it’s multiple phases of life where you really get to come into your own.

For a growing number of Australians this new chance for a longer life, and new financial freedom via superannuation, is reshaping how midlife and retirement years are viewed.

And superannuation arrived just at the right time to make this possible.

In fact, superannuation climbing to meaningful contribution rates is what has given us the financial means to truly change things up and actually start to choose what those extra years can look like. For the first time, reaching your sixties doesn’t have to mean the beginning of the end. It can mean the beginning of something entirely new, fresh and exciting.

This article continues. It was published in The Age and The Sydney Morning Herald on Saturday 20th June 2026. Read the whole article here. Note - it has a sign-up gate but no paywall.

Over the past month, we’ve talked about planning for retirement, finding purpose beyond work and creating a life you’ll actually want to wake up to.

But there is one final piece of the puzzle: how do you pay for it?

In the final episode of our New Rhythm of Retirement series with Aware Super, I’m joined once again by Peter Hogg and Lynda Cross to tackle the money mechanics of retirement.

We discuss one of the biggest psychological adjustments retirees face: moving from the predictable rhythm of a regular paycheck to funding your lifestyle from your own savings. We also explore the opportunities hidden within your biggest assets, including your super and family home, and unpack some of the strategies that can help stretch your retirement income further.

As we know, retirement isn’t just about having enough money. It’s also about having the confidence to use it.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

I reckon the strike rate on dodgy advice from FA’s would be higher than the 30% AI rate 😃

I used AI to assemble a complete list of questions for my sister to ask the FA they saw.

He was not impressed…😎 His expectation was that they cough up something like $12k each, plus ongoing fees and for them to be happy with whatever high fee crappy wrap product he could come up with.

They got out of there asap.

They also tried to use ARTs free advice, but as soon as they got past, what is your name and age he was trying to sign them up to see a paid service 😡, despite their advertising saying you can get detailed advice as long as it is related to their super products.

Thank you for your comments on AI. For me, it is becoming invaluable. It does require you to provide sufficient context and then start asking clear questions. If you ask general stuff then you get poor answers. I’ve used it to create a dashboard for our SMSF that includes points for discussion with our financial advisor. It certainly helps test the advice you receive.