What sort of investment returns does your retirement plan actually need?

And, in the Nine Newspapers this weekend "The budget killed my daughter’s property plan. Here’s what we’ll do instead"

In this edition: It’s a juicy one

Feature: What sort of investment returns does your retirement plan actually need?

From Bec’s Desk: A new gym and a course that’s booking fast

The Age and Sydney Morning Herald: The budget killed my daughter’s property plan. Here’s what we’ll do instead

Prime Time: ‘Is housing still a good investment?’ with Dr Shane Oliver

Ad - Our next Epic Retirement flagship course is booking fast

The ultimate retirement planning course

It’s here! Our new Spring edition of the How to Have an Epic Retirement Flagship Course has officially gone on sale a week ago at the 25% off earlybird price. And you’ve flooded us with bookings.

It’s a six week program, designed to help you step through six weeks, 8.5 hours of retirement lessons, about everything you need to understand to navigate retirement with confidence.

It’s a course that gets rave reviews. And we only run it four times a year. Last time we completely sold out (of books and workbooks) so we had to shut the doors early!

The new program has been fully updated with all the new changes that arrived on 1 July. We’ve also launched a new website, so you can pop on over and read all about it, and book your place.

There’s a 25% off Earlybird Deal on now, for the first 200 people who book. So get in there, check out all the inclusions (it’s a huge list) and lock down your place as they sold out well and truly last time. There’s also a detailed brochure you can download.It sells out. It gets rave reviews. And it’s just been fully updated with every change that landed on July 1.

If you’ve been thinking you might - nows the day to book.

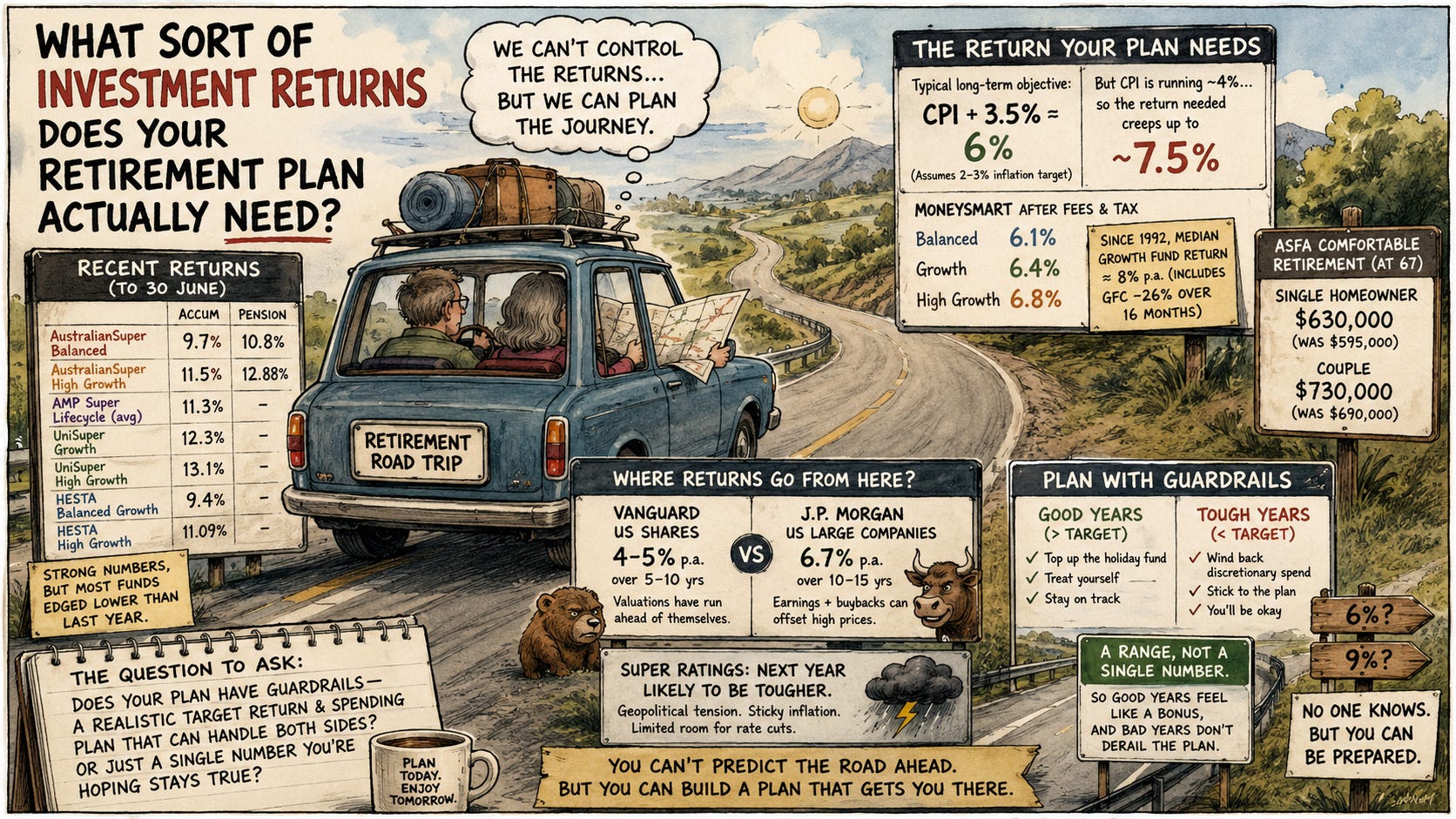

What sort of investment returns does your retirement plan actually need?

The financial year just closed, and the fund-by-fund results are starting to land. AustralianSuper’s Balanced option came in at 9.7% in accumulation and 10.8% for pension accounts for the year to 30 June, up slightly from 9.5% in accumulation and 10.4% in pension the year before. Their High Growth option did 11.5% in accumulation and 12.88% in pension. AMP Super’s lifecycle funds have delivered 11.3% returns for the financial year. Unisuper’s Growth option returned 12.3%, High Growth 13.1%. HESTA’s Balanced Growth option hit 9.4% its fourth year running above 9% and High Growth 11.09%.

These really are strong numbers, especially given the year we’ve just had with an oil shock and geopolitial tension combined. But there’s one detail that the headlines are skipping over: most funds actually came in a little lower than the year before. AustralianSuper, UniSuper and Rest were among the few that improved on FY25. Everyone else eased off the peak a little, even while still posting a good year by any normal measure.

So if your balance looks better than you expected, that’s great, take the win. But it’s worth being honest about which of those two stories you’re actually in, the ones still climbing, or the ones that had a slightly softer year than last time. Either way, neither tells you much about what comes next. And that’s what I really want to get you thinking about today.

The typical long-term return objective for a growth super fund, the number the whole strategy is built around, is CPI plus 3.5%. Funds set that against the RBA’s 2 to 3% inflation target, (not whatever CPI happens to be doing this month), and worked through that way it lands at just over 6% a year. Worth knowing CPI isn’t behaving right now though. It was running at 4% for the year to May, well above target. If that sticks around, the return your fund actually needs to hit that same real objective creeps up too, closer to 7.5% than 6%. That’s also close to where the government’s own Moneysmart calculator sets its assumptions: 6.1% for Balanced, 6.4% for Growth, 6.8% for High Growth, after fees and tax, numbers that only really hold if inflation behaves the way the long-term target assumes it will. Since compulsory super started in 1992, the median growth fund has actually averaged closer to 8% a year, but that includes the GFC, when growth funds lost around 26% over sixteen brutal months. The good years and the bad years average out to 8%. Most plans are only built to need 6% - unless you’ve overridden the numbers with higher expectations.

Most of you who read this newsletter regularly, would already be aware that the Association of Superfunds, ASFA moved their headline ‘how much do you need to retire in comfort’ numbers for the first time in three years just recently. A single homeowner now needs $630,000 at 67 for a comfortable retirement, up from $595,000. A couple needs $730,000, up from $690,000. Their reasoning was straightforward: living costs have outpaced what the Age Pension covers, so more of the job falls back on your own super. It’s got an important job to do - but where do we think super returns are heading, and should they really be expected to last at these high levels?

I wanted a second opinion on where returns actually go from here, and what we really should be planning for, particularly if the world stopped delivering near-double-figure returns, so I looked at what the big global investment houses are forecasting, and they don’t agree with each other at all. Vanguard reckons US shares, which make up a big slice of most growth options, will only manage 4 to 5% a year over the next five to ten years, on the view that tech valuations have run ahead of themselves. J.P. Morgan, looking at the same market, forecasts 6.7% for US large companies over ten to fifteen years, arguing strong earnings and buybacks can keep offsetting high prices even as the froth comes off.

These are two of the best resourced research teams in the world, who use the same data, yet they are more than two points apart. Closer to home, SuperRatings has already flagged this coming year as likely to be tougher, pointing to rising geopolitical tension and an inflation picture that isn’t giving much room for local rate relief.

Of course, none of this is a reason to change anything about your super today. It’s a reason to check what you’re actually banking on the markets and your fund returning you versus what the reality could be. The last four years have been a terrific run for funds. And while they are worth enjoying, it might not be smart to build your retirement decisions around returns like this holding up.

This is exactly why I like the idea of guardrails in how we plan for spending in retirement, rather than picking one return number and hoping it holds. Think of it a bit like a road trip where you have a rough budget in mind. If you have a great year and come in under budget, you top up the holiday fund or treat yourself a bit more. If a year’s tighter than expected, you already know beforehand what you’ll wind back on discretionary spending, rather than working it out in a panic halfway through. Nobody can tell you in advance whether the next stretch looks like 6% or 9%, not even the people paid quite a lot to guess. What you can do is build a plan with a bit of give in it either way, so a good year feels like a bonus and a bad year still turns out okay.

So ask yourself this week: does your plan actually have guardrails - a target return and spending number that’s achieveable - or just a single number you’re hoping stays true? You don’t need the answer today - just think about the returns you’re relying on, and make sure your plan still holds up if markets don’t return high single figures or even double digits every year.

Want to read more, I have two books - How to Have an Epic Retirement and if you’re not ready for retirement, Prime Time: 27 Lessons for the New Midlife.

This week I started at a new gym. Yep, I’ve stepped up to small group training and I can now officially feel every muscle in my body - out loud. I hunted around to find a gym where I can be supervised and coached as I do progressive lifting, something the science says is important as we age. I’ll report back on the process. But week 1 = good! Any of you done the same? I was encouraged by my interview with Van Marinos on the podcast a few weeks ago.

THE EPIC RETIREMENT COURSE

Outside of this, on the work front, we’ve been overwhelmed by your bookings of the upcoming Epic Retirement course. There’s still a few seats left on our Earlybird deal which has 200 places. Then the price will go back to the RRP. So don’t delay - you know I want everyone to get the best deal available. Download a brochure here and book your place.

MELBOURNE RIGHTSIZING!

I’m heading to Sydney and Melbourne this week, just briefly. In Melbourne I’ll be presenting at a really interesting event on downsizing into luxury apartments. I’m excited. The event is being held by Lowe Living. If it interests you - click here to learn more and register your place. I’m speaking with the property economics gurus from Urbis.

HESTA’S EPIC RETIREMENT COURSE

We’re launching a new Epic Retirement program for HESTA members in the next couple of days. So if you’re a HESTA member - check it out here. It’s a great course. You need to be a member of HESTA to access it. And there’s limited places - so don’t dilly dally!

—

And Bec’s Epic Bucket List Holidays

Nearly 1000 of you registered your interest for my Epic Bucket List Trips. That’s blown me away. These are going to be our commmunity trips to real bucket list destinations. And now, we’re surveying on the potential destinations for year 1 and getting a feel for what is of real interest. Fiona Dalton, the Epic travel guru is leading the way on this, picking the adventures to ask you about.

I mean real handpicked bucket list stuff. Active and experience-first. And never the same destination twice. If you’re on the EOI list, we’ll be emailing you a wish list to explore what you’d want to do out of our ideas in the week ahead. And if you haven’t put your name on the list yet - Express your interest here - no obligation. Then you can do the survey after.

Author, podcast host, columnist, retirement educator, and guest speaker

The budget killed my daughter’s property plan. Here’s what we’ll do instead

When the budget hit in May, I was starting a book and a social media series with my 22-year-old daughter on how we can give our adult kids an epic start in life without just handing them a wad of cash.

She’s been learning the foundations of budgeting, saving and investing across the kitchen table with me since she returned from her gap year last year. And she’s been studying, working and saving hard for her next meaty goal – buying her first home.

We’d done the maths, and she was fairly confident that when she graduated from university next year, that she’d be able to use a couple of years’ living in our family home well, saving a healthy deposit, investing it diligently, and be prepared for her first foray into property within a year or two of graduating.

She had a plan to get on to the housing ladder by about 25 years old, albeit in an investment property because buying a unit she could afford the mortgage on while living in it as a single person, on a graduate teacher’s wage, was nigh on impossible.

She was then going to take her time living at home to see if she could build some equity in that investment property that could be used later to buy her first real home.

When the federal budget came, that strategy became completely unviable.

This article continues… It is published in The Age and Sydney Morning Herald on Saturday 11th July 2026. Read the whole article here, without a paywall.

‘Is housing still a good investment?’ with Dr Shane Oliver

There is so much uncertainty since the budget, and we’re starting to see and feel the economic fallout.

People are asking whether they should still invest in property? Whether the share market will continue to perform? Or whether they should simply sit on cash and wait for things to settle down.

We’re in a very different investment environment from the one we’ve become used to over the past decade. And so this week, I invited one of Australia’s most respected economists, Dr Shane Oliver, back to Prime Time to help us make sense of it all.

Together, we unpack what the budget changes are already starting to mean for property investors, first home buyers and anyone trying to build wealth for retirement.

We also discuss Australia’s productivity problem, where interest rates are heading, how the share market is likely to respond and why Shane believes it’s important not to lose sight of the long-term picture.

So, whether you’re still building wealth or preparing to retire, this is one of those conversations that helps separate the headlines from what’s actually happening in the economy.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Would be better if you could include figures for non-homeowners as well in these posts. There are a lot of us out here who don’t own our own homes!

I am loving the graphics Becs and what a great article, love that statement, "we can't control the returns, but we can plan the journey" put our efforts into the things we can control🙌